Company announces year-over-year revenue, production, and operating fleet increases; 2024 portfolio highlights; valuation adjustments; and business restructuring

Key Takeaways

- Amid challenging market conditions, including inflationary pressures and macro uncertainty, Greenbacker announces decrease in NAV.

- Charles Wheeler retires as CEO; Dan de Boer assumes position of interim CEO; Robert Brennan appointed Chairman of the Board.

- Company institutes additional cost saving measures, including 10% reduction in workforce; operating expenses expected to reduce by $12 million, or 20%, by 2026.

- Board of Directors authorizes review of strategic alternatives to enhance shareholder value.

- Total operating revenue in 2024 increased by 16% year-over-year, to $210 million.

- Operating fleet grew by 8%, with 22 new solar energy assets in operation representing 117 MW of additional power production capacity.

- Annual power production increase of 23% driven by new solar assets combined with Company’s milestone wind repowers.

- Greenbacker’s fleet of clean energy assets generated 2.7 billion kilowatt-hours of power, enough to power 250,000 US homes.

NEW YORK, April 1, 2025 – Greenbacker Renewable Energy Company LLC (“Greenbacker,” “GREC,” or the “Company”), an energy transition-focused investment manager and independent power producer, has announced financial results for 2024, including year-over-year increases in annual revenue, operating capacity, and clean energy generation.1

Market conditions, inflationary pressures, and re-underwriting process determined adjusted NAV

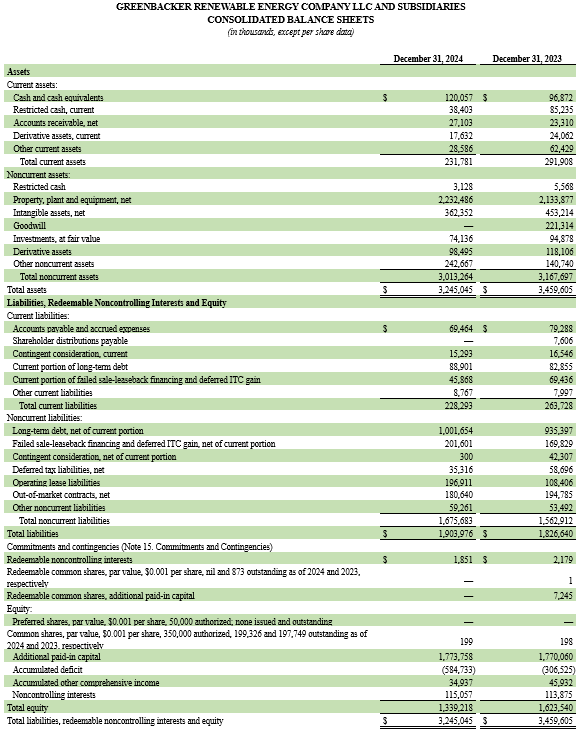

With the renewable energy sector at a critical juncture, during 2024 Greenbacker initiated a detailed, multi-quarter re-underwriting process prior to releasing its December 31, 2024 net asset value (“NAV”), in which the Company evaluated the expected future performance of the assets in its portfolio relative to their historical performance, while also taking into account the impact of current market conditions. As a result, GREC adjusted its aggregate NAV as of December 31, 2024 to $5.03 per share, a 35.5% decrease relative to the September 30, 2024 NAV of $7.81 per share.

Several factors contributed to the Company’s NAV revision. Inflationary pressures, supply chain imbalances, and increasing insurance costs due to heightened climate risk contributed to a significant increase in operating costs. New clean energy generation projections from independent engineers based on recent industry data have provided additional insight, replacing earlier projections that had been obtained during a period with limited historical data available and diverged relative to actual production. Additionally, there continues to be uncertainty around potential changes to the Inflation Reduction Act and the threat of additional tariffs, both of which are impacting the near-term outlook for renewables.

These headwinds contributed to a challenging market environment and downward pressure in renewable energy asset pricing across the sector, which Greenbacker saw reflected through both market sale processes and a comprehensive asset-by asset-review.

At the project level, the Company continues to maintain financial stability, resulting in strong financial coverage ratios. Additionally, at the firm level, Greenbacker continues to maintain sufficient overall liquidity and receive ongoing support from its leading project financing partners.

Organizational restructuring executed to increase operational efficiencies

Greenbacker is announcing an organizational restructuring designed to streamline operations, reduce costs, and better position the Company to capitalize on future market opportunities and deliver value to shareholders.

As part of these changes, Charles Wheeler is retiring from his role as Chief Executive Officer (“CEO”) and Chairman of the Greenbacker Board of Directors (“Board”), effective April 1, 2025. Chief Investment Officer and Head of Infrastructure Dan de Boer has been named interim CEO, effective April 1, 2025, and Director Robert Brennan has been appointed Chairman of the Board. The Greenbacker Board is considering both external and internal candidates for the role of a permanent CEO, which is expected to be confirmed no later than the end of Q2 2025. Wheeler will continue to serve as a member of the Board until the earlier of December 31, 2025 and the date on which a permanent replacement CEO has been appointed.

Wheeler, who is also one of Greenbacker’s Co-Founders, spoke about his retirement and Greenbacker’s future:

“14 years ago, with a group of like-minded individuals, I created Greenbacker with the goal of providing an investment vehicle that would enable ordinary American investors to participate in the renewable energy revolution. We’ve built Greenbacker into a business that is contributing to the transition to clean energy with hundreds of projects representing more than 3.6 gigawatts2 of clean power generation capacity across the country.

Given current market conditions, changes are needed to best position Greenbacker to benefit from future market opportunities. I believe that Dan and Greenbacker’s other leaders are the right team to guide us through this period while promoting our mission to empower a sustainable world.”

De Boer has been with Greenbacker since 2023 and brings nearly two decades of experience in private equity and renewable energy investing, with prior leadership roles and positions at Allianz Capital Partners, Onyx Renewable Partners within Blackstone Energy Partners, and D.E. Shaw Renewable Investments.

In addition to restructuring the leadership team, the Company has progressed several cost savings initiatives, including a reduction of approximately 10% of its workforce, effective March 31, 2025. Greenbacker anticipates that the reduction in force and other operational efficiency efforts that began in mid-2024 will reduce overhead expenses by $12 million, or 20%, by 2026.

“We want to recognize the impact that this decision has on the careers and lives of the individuals at Greenbacker,” said interim CEO, Dan de Boer. “We value our people and employed care and thoughtfulness as we attempted to balance our business requirements with any adverse impact to our team. While difficult, we believe that taking these measures will better position the firm to achieve long-term growth.”

Additionally, the Company has identified opportunities to recycle capital within the portfolio by pursuing targeted non-core asset sales.

Annual total operating revenue topped $210 million, as Company continued to move assets into operation, contributing to year-over-year production increase of 23%

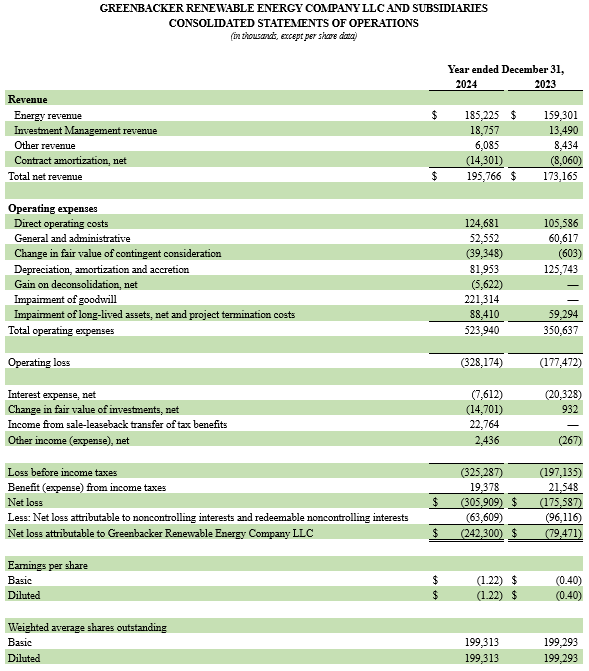

During 2024, Greenbacker increased total operating revenue3 by $29 million, or 16% year-over-year, to over $210 million.

Revenue from the sale of clean energy within Greenbacker’s independent power producer (“IPP”) business segment totaled $185.2 million in 2024, of which $155.0 million, or approximately 84%, came from the Company’s long-term power purchase agreements (“PPAs”).

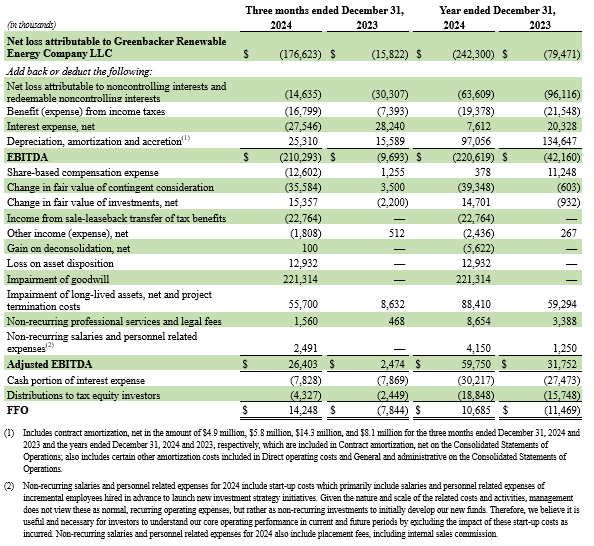

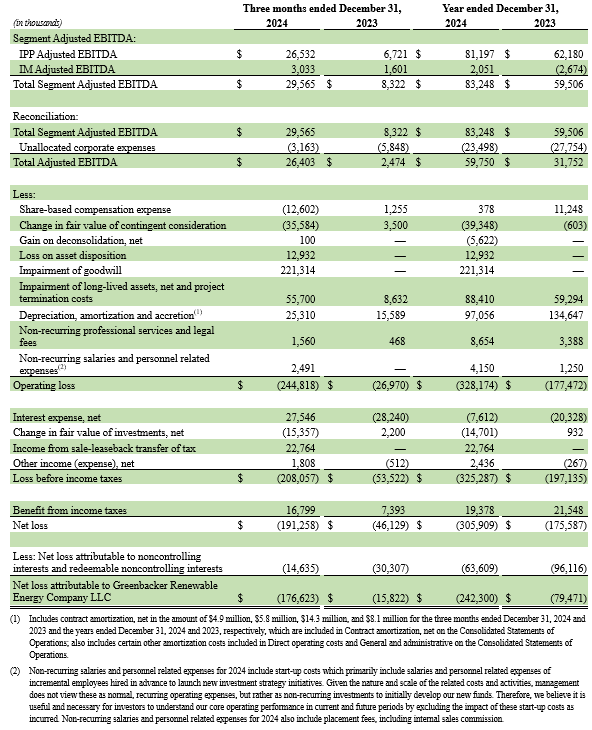

For 2024, the net loss attributable to Greenbacker was $(242.3) million and Adjusted EBTIDA4 was $59.8 million, representing year-over-year changes of (205)% and 88%, respectively. The net loss was primarily the result of goodwill impairment charges, driven by a deterioration in macroeconomic conditions, as well as by depreciation, amortization, and other impairment charges in the period.

GREC increased its operating fleet size by 8% in 2024, which included placing 22 new solar energy assets into operation, accounting for 117 MW of additional power production.5 Additionally, the three wind assets strategically taken offline during portions of 2023 for repowering (i.e., retrofitting with new, more efficient equipment) had all returned to full operation producing power by early 2024.

In total, GREC’s new operating solar assets and repowered wind portfolio drove an annual power production increase of 23% year-over-year,6 as the Company’s fleet of clean energy assets generated 2.7 billion kilowatt-hours of power, enough to power over 250,000 US homes.7

| GREC Operating Fleet | 2024 | 2023 | YoY Increase (total) | YoY Increase (%) |

| Clean power produced by solar assets (MWh) | 1,504,580 | 1,256,183 | 248,397 | 20% |

| PPA revenue generated by solar assets ($M) | $ 87.8 | $ 74.1 | $ 13.6 | 18% |

| Clean power produced by wind assets (MWh) | 1,236,431 | 978,236 | 258,195 | 26% |

| PPA revenue generated by wind assets ($M) | $ 65.8 | $ 53.9 | $ 11.9 | 22% |

| Total clean power generated by wind and solar assets (MWh) | 2,741,011 | 2,234,419 | 506,592 | 23% |

| Total PPA operating revenue generated by wind and solar assets ($M) | $ 153.5 | $ 128.0 | $ 25.5 | 20% |

Some figures may not add to stated totals due to rounding. Total clean power generated does not include power generated from biomass facility during 2023 and a portion of 2024, nor does it include assets in which the Company holds a preferred equity position.

Greenbacker secures nearly $1 billion financing for largest solar farm in New York State; completes $437 million financing for milestone wind repowers; and completes targeted non-core asset sale

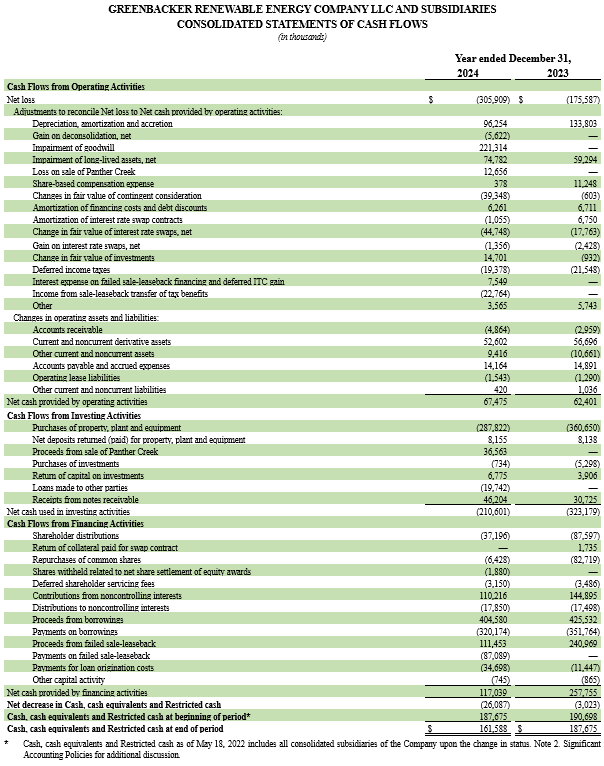

Throughout 2024, Greenbacker made substantial progress on one of its core objectives: securing the capital necessary for the construction of its remaining pre-operating assets—and converting those projects into revenue-generating operating assets selling electricity. The Company also continued to receive robust support from its project finance partners, enabling it to reach significant milestones over the year.

In particular, Greenbacker secured nearly $1 billion in financing for the acquisition, construction and operation of its 674 MW Cider solar farm, the largest solar energy project in the state of New York to date. Cider also represents both Greenbacker’s largest clean energy asset to date and the largest project financing in Company history (for which it was awarded Proximo Infrastructure’s 2024 Solar Deal of the Year).

The construction financing represented $869 million from six of the world’s top financial institutions, including ongoing Greenbacker partners MUFG, KeyBanc Capital Markets and Wells Fargo, as well as first-time partnerships with ING Capital LLC, Intesa Sanpaolo S.p.A., New York Branch and Societe Generale. The Company also closed on an $81 million development loan with Voya Investment Management, its first partnership with the global investment manager.

Greenbacker additionally completed $437 million in financing for its wind repower portfolio. GREC was able to create additional value from existing assets by updating the turbine blades, hubs, and nacelles at three wind projects in its Midwestern fleet. To finance the repowering, the Company collaborated with lending partner Bayerische Landesbank to secure $81.5 million in construction bridge loan facilities, as well as long-term debt and tax equity financing from Huntington National Bank, via sales leasebacks totaling $355.7 million.

Also in 2024, Greenbacker completed the sale of its 54 MW Panther Creek pre-operating wind asset to an affiliated sustainable infrastructure-focused platform. The asset sale illustrated GREC’s ability to develop large clean energy assets through late-stage development, a key component of its go-forward strategy, while its affiliate platform viewed the project as an opportunity to add a fully developed, high cash-yielding asset, in line with its investment mandate.

Long-term contracted cash flows with investment-grade counterparties

As of December 31, 2024, the Greenbacker operating fleet represented approximately 1.6 gigawatts of total clean power generation and storage capacity, spanning over 30 states, territories, districts and provinces. Due to its size and geographic footprint, GREC’s operating fleet was listed among Solarplaza’s 2025 Top 50 Operating Solar Portfolios in North America.

At the end of 2024, over 93% of Greenbacker’s entire portfolio of operating and pre-operating clean energy projects were currently, or will be when completed, selling power to investment-grade counterparties, including utilities, municipalities, and corporations, under long-term power purchase agreements (“PPAs”). The portfolio had approximately 17.4 years of contracted cash flows associated with these PPAs.

Review of strategic alternatives

In addition to the other measures to reduce costs, operate more efficiently, and promote a path to better outcomes for its investors, the Greenbacker Board has authorized the Company to conduct a comprehensive review of strategic alternatives.

In regard to this review, the Board will consider a full range of operational and financial alternatives. A strategic review may result in Greenbacker securing additional capital to continue executing on its business plan: acquiring, owning, and operating a fleet of sustainable infrastructure assets that the Company efficiently manages to create both value and potential liquidity options for its shareholders.

“During 2024, Greenbacker closed on the Cider deal, completed our milestone wind repowers, and brought 117 MW of additional capacity online, showcasing how we can utilize additional capital while continuing to deliver on our core focus,” de Boer said. “We believe current valuations in the renewables sector do not align with the supportive fundamentals driving the energy transition, leading to a compelling inflection point for renewable infrastructure investment. In short: we believe this is one of the better times to be investing in the energy transition.”

Company’s investments produce power, abate carbon emissions, conserve water, and support green jobs

As of December 31, 2024, Greenbacker’s clean energy assets had cumulatively produced more than 11 million MWh of clean power since January 2016, abating over 7 million metric tons of carbon8 and saving nearly 8 billion gallons of water.9 Greenbacker’s fleet of operating and pre-operating projects currently support, or are expected to support, thousands of green jobs.10

Additional information regarding the Company’s impact can also be found in Greenbacker’s latest impact report.

Forward-Looking Statements

This press release contains forward-looking statements, including those that relate to our search for a permanent Chief Executive Officer, our strategy and initiatives and our expectations for growth, within the meaning of the federal securities laws. Forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that may cause the actual results to differ materially from those anticipated at the time the forward-looking statements are made. The potential risks and uncertainties that could cause our actual results, performance or achievements to differ from the predicted results, performance or achievements include, among others, difficulties or delays we encounter in identifying a permanent Chief Executive Officer; our ability to execute on, and achieve the expected benefits from, our operational and strategic initiatives; our inability to realize the expected reduction in overhead expenses as a result of our reduction in force; volatility of the global financial markets and uncertain economic conditions, including changes in interest rates, inflationary pressures, recessionary concerns or global supply chain issues; public response to and changes in the local, state and federal regulatory framework affecting renewable energy projects; risks associated with changes in the fair value of our investments and the methods we use to estimate the fair value of our assets; and other risks and uncertainties discussed in our most recent Forms 10-K, 10-Q and 8-K filed with or furnished to the SEC. Although Greenbacker believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that the expectations will be attained or that any deviation will not be material. Greenbacker undertakes no obligation to update any forward-looking statement contained herein to conform to actual results or changes in its expectations.

Non-GAAP Financial Measures

In addition to evaluating the Company’s performance on a U.S. GAAP basis, the Company utilizes certain non-GAAP financial measures to analyze the operating performance of our segments as well as our consolidated business. Each of these measures should not be considered in isolation from or as superior to or as a substitute for other financial measures determined in accordance with U.S. GAAP, such as net income (loss) or operating income (loss). The Company uses these non-GAAP financial measures to supplement its U.S. GAAP results in order to provide a more complete understanding of the factors and trends affecting its operations.

Adjusted EBITDA

Adjusted EBITDA is a non-GAAP financial measure that the Company uses as a performance measure, as well as for internal planning purposes. We believe that Adjusted EBITDA is useful to management and investors in providing a measure of core financial performance adjusted to allow for comparisons of results of operations across reporting periods on a consistent basis, as it includes adjustments relating to items that are not indicative on the ongoing operating performance of the business.

Adjusted EBITDA is a performance measure used by management that is not calculated in accordance with U.S. GAAP. Adjusted EBITDA should not be considered in isolation from or as superior to or as a substitute for net income (loss), operating income (loss) or any other measure of financial performance calculated in accordance with U.S. GAAP. Additionally, our calculations of Adjusted EBITDA may not be comparable to similarly titled measures reported by other companies.

Funds From Operations (FFO)

FFO is a non-GAAP financial measure that the Company uses as a performance measure to analyze net earnings from operations without the effects of certain non-recurring items that are not indicative of the ongoing operating performance of the business. FFO is calculated using Adjusted EBITDA less the impact of interest expense (excluding the non-cash component) and distributions to tax equity investors under the financing facilities associated with our IPP segment.

The Company believes that the analysis and presentation of FFO will enhance our investor’s understanding of the ongoing performance of our operating business. The Company considers FFO, in addition to other GAAP and non-GAAP measures, in assessing operating performance and as a proxy for growth in distribution coverage over the long term.

FFO should not be considered in isolation from or as a superior to or as a substitute for net income (loss), operating income (loss) or any other measure of financial performance calculated in accordance with U.S. GAAP.

General Disclosure

This information has been prepared solely for informational purposes and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, or to participate in any trading or investment strategy. The information presented herein may involve Greenbacker’s views, estimates, assumptions, facts, and information from other sources that are believed to be accurate and reliable and are, as of the date this information is presented, subject to change without notice.

Non-GAAP Reconciliations

Adjusted EBITDA

Adjusted EBITDA is a non-GAAP financial measure that the Company uses as a performance measure as well as for internal planning purposes. We believe that Adjusted EBITDA is useful to management and investors in providing a measure of core financial performance adjusted to allow for comparisons of results of operations across reporting periods on a consistent basis as it includes adjustments relating to items that are not indicative of the ongoing operating performance of the business.

The Company defines Adjusted EBITDA as net income (loss) before: (i) interest expense; (ii) income taxes; (iii) depreciation expense; (iv) amortization expense (including contract amortization); (v) accretion; (vi) impairment of long-lived assets; (vii) amounts attributable to our redeemable and non-redeemable noncontrolling interests; (viii) unrealized gains and losses on financial instruments; (ix) gains and losses for asset dispositions; (x) other income (loss); and (xi) foreign currency gain (loss). Additionally, the Company further adjusts for the following items described below:

• Share-based compensation is excluded from Adjusted EBITDA as it is different from other forms of compensation as it is a non-cash expense and is highly variable. For example, a cash salary generally has a fixed and unvarying cash cost. In contrast, the expense associated with an equity-based award is generally unrelated to the amount of cash ultimately received by the employee, and the cost to the Company is based on a share-based compensation valuation methodology and underlying assumptions that may vary over time;

• The change in fair value of contingent consideration, which is related to the Acquisition, is excluded from Adjusted EBITDA, if any such change occurs during the period. The non-cash, mark-to-market adjustments are based on the expected achievement of revenue targets that are difficult to forecast and can be variable, making comparisons across historical and future quarters difficult to evaluate;

• Beginning 2024, start-up costs associated with new investment strategies is excluded from Adjusted EBITDA. The Company evaluates new investment strategies on a regular basis and excludes start-up cost from Adjusted EBITDA until such time as a new strategy is determined to form part of the Company’s core investment management business.

• Beginning 2024, placement fees, including internal sales commissions, related to fundraising efforts based on the capital raised, are excluded from Adjusted EBITDA. By excluding these fundraising-related fees from Adjusted EBITDA, we focus on core operational performance, separate from capital raising efforts, which might vary significantly from period to period.

• Other costs that are not consistently occurring, not reflective of expected future operating expense and provide no insight into the fundamentals of current or past operations of our business are excluded from Adjusted EBITDA. This includes costs such as professional services and legal fees, and other non-recurring costs unrelated to the ongoing operations of the Company.

Adjusted EBITDA is a performance measure used by management that is not calculated in accordance with U.S. GAAP. Adjusted EBITDA should not be considered in isolation from or as superior to or as a substitute for net income (loss), operating income (loss) or any other measure of financial performance calculated in accordance with U.S. GAAP. Additionally, our calculations of Adjusted EBITDA may not be comparable to similarly titled measures reported by other companies.

FFO

FFO is a non-GAAP financial measure that the Company uses as a performance measure to analyze net earnings from operations without the effects of certain non-recurring items that are not indicative of the ongoing operating performance of the business.

FFO is calculated using Adjusted EBITDA less the impact of interest expense (excluding the non-cash component) and distributions to Tax Equity Investors under the financing facilities associated with our IPP segment. The Company excludes these distributions as these are not recorded within Adjusted EBITDA and is therefore not a component of our earnings from operations.

The Company believes that the analysis and presentation of FFO will enhance our investors’ understanding of the ongoing performance of our operating business. The Company considers FFO, in addition to other GAAP and non-GAAP measures, in assessing operating performance and as a proxy for growth in distribution coverage over the long-term.

Adjusted EBITDA and FFO should not be considered in isolation from or as a superior to or as a substitute for net income (loss), operating income (loss) or any other measure of financial performance calculated in accordance with U.S. GAAP.

The following table reconciles Net loss attributable to Greenbacker Renewable Energy Company LLC to Adjusted EBITDA and FFO:

Adjusted EBITDA for the year ended December 31, 2024 has not been adjusted for the charges of $16.6 million incurred as part of a settlement agreement with a third-party vendor due to the termination of the existing purchase contract in order to acquire the solar panels needed for our development and construction pipeline from a different vendor with significantly better economic proposition due to reduced expected cash outlays.

About Greenbacker Renewable Energy Company

Greenbacker Renewable Energy Company LLC is a publicly reporting, non-traded limited liability sustainable infrastructure company that both acquires and manages income-producing renewable energy and other energy-related businesses, including solar and wind farms, and provides investment management services to other renewable energy investment vehicles. We seek to acquire and operate high-quality projects that sell clean power under long-term contracts to high-creditworthy counterparties such as utilities, municipalities, and corporations. We are long-term owner-operators, who strive to be good stewards of the land and responsible members of the communities in which we operate. Greenbacker conducts its investment management business through its wholly owned subsidiary, Greenbacker Capital Management, LLC, an SEC-registered investment adviser. We believe our focus on power production and asset management creates value that we can then pass on to our shareholders—while facilitating the transition toward a clean energy future. For more information, please visit https://greenbackercapital.com.

About Greenbacker Capital Management

Greenbacker Capital Management LLC is an SEC registered investment adviser that provides advisory and oversight services related to project development, acquisition, and operations in the renewable energy, energy efficiency, and sustainability industries. For more information, please visit www.greenbackercapital.com.

1 The financial and portfolio metrics set forth herein are unaudited and subject to change. Data as of December 31, 2024. Total assets and megawatts statistics include those projects where we have contracted for the acquisition of the project pursuant to a Membership Interest Purchase Agreement (“MIPA”).

2 Includes pre-operating and operating assets across combined GREC and GREC II portfolios. Data as of December 31, 2024.

3 Total operating revenue excludes non-cash contract amortization, net.

4 Adjusted EBITDA is a non-GAAP financial measure that the Company uses as a performance measure, as well as for internal planning purposes. We believe that Adjusted EBITDA is useful to management and investors in providing a measure of core financial performance adjusted to allow for comparisons of results of operations across reporting periods on a consistent basis, as it includes adjustments relating to items that are not indicative on the ongoing operating performance of the business. See “Non-GAAP Financial Measures” for additional discussion. Adjusted EBITDA is unaudited. See the Company’s 10-K filed with the SEC for additional financial information and important related disclosures.

5 Data as of December 31, 2024. Total assets and megawatts statistics include those projects where we have contracted for the acquisition of the project pursuant to a Membership Interest Purchase Agreement (“MIPA”). The financial and portfolio metrics set forth herein are unaudited and subject to change

6 Does not include power generated from biomass facility during 2023 and a portion of 2024, and also does not include assets in which the Company holds a preferred equity position

7 Frequently Asked Questions (FAQs) – U.S. Energy Information Administration (EIA)

8 Data is as of December 31, 2024. When compared with a similar amount of power generation from fossil fuels. Carbon abatement is calculated using the EPA Greenhouse Gas Equivalencies Calculator which uses the Avoided Emissions and generation Tool (AVERT) US national weighted average CO2 marginal emission rate to convert reductions of kilowatt-hours into avoided units of carbon dioxide emissions.

9 Data is as of December 31, 2024. Water saved by Greenbacker’s clean energy projects is compared to the amount of water needed to produce the same amount of power by burning coal. Gallons of water saved are calculated based on Operational water consumption and withdrawal factors for electricity generating technologies: a review of existing literature – IOPscience, J Macknick et al 2012 Environ. Res. Lett. 7 045802.

10 Data is as of December 31, 2024. Green jobs calculated using The National Renewable Energy Laboratory (NREL) State Clean Energy Employment Projection Support, nrel.gov.